Payday Super Is Coming: What Employers Need to Know

Summary:

From 1 July 2026, the way employers pay superannuation for their employees will change. These reforms, known as Payday Super, are designed to align super payments more closely with employees’ pay cycles and will affect how businesses manage payroll, cash flow and compliance.

What’s changing from 1 July 2026?

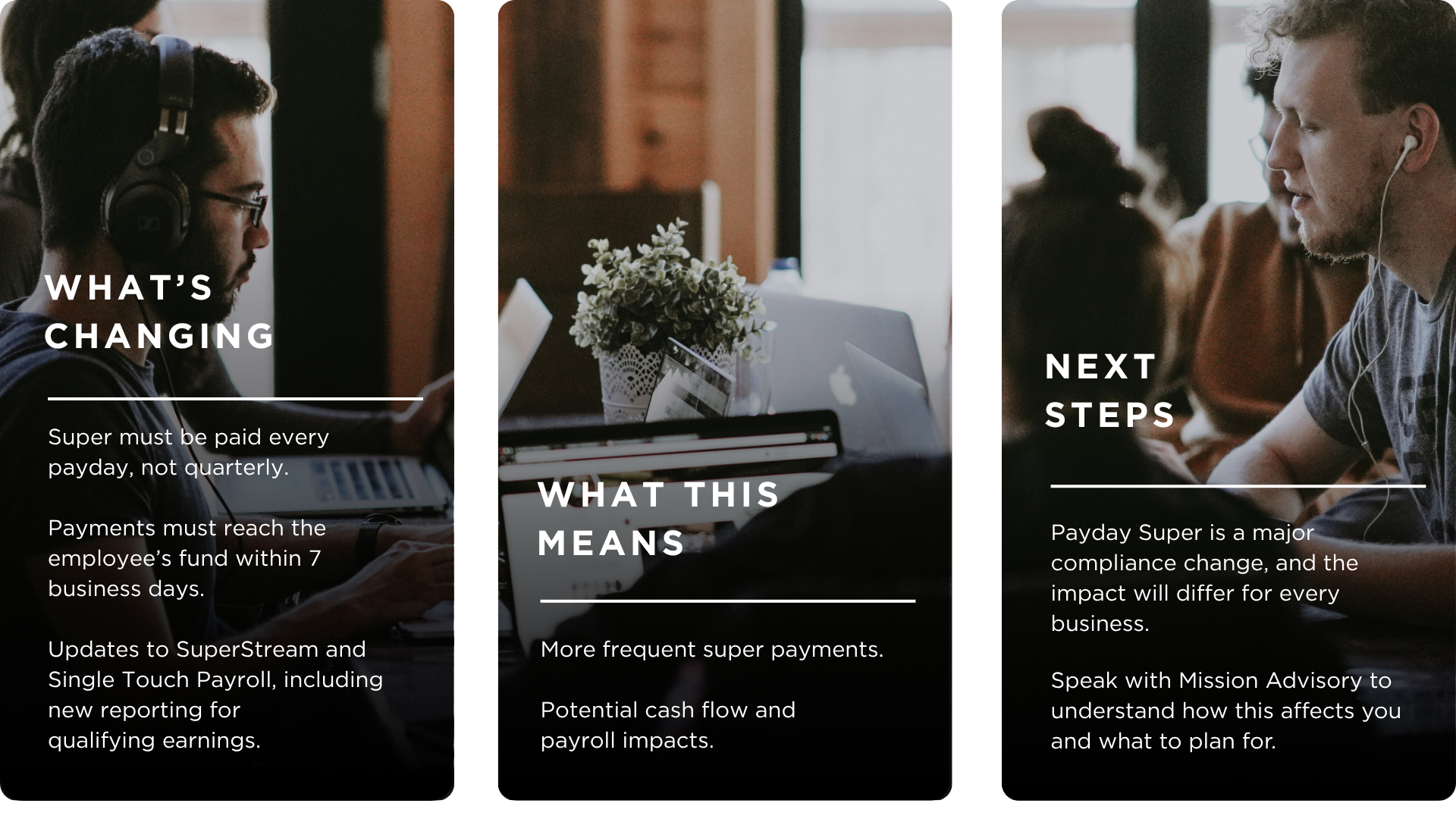

Under the new rules, employers will be required to pay super guarantee (SG) contributions each time employees are paid, rather than making contributions on a quarterly basis. Importantly, the employee’s super fund must receive the payment within seven business days of payday. If payments are received later than this, penalties may apply.

This represents a significant shift from the current system and will require many employers to rethink how and when super is paid.

Changes to reporting and systems

Alongside the move to Payday Super, the ATO is updating several key systems that employers already use.

SuperStream will be enhanced to include clearer error messages and a new member verification request, which is intended to reduce issues such as failed or misdirected super payments.

Single Touch Payroll (STP) reporting will also change. Employers will be required to report not only their superannuation liability, but also a new measure called qualifying earnings.

These updates may require changes to payroll software and internal processes. However, it is worth noting that ‘Xero superannuation’ is built into ‘Xero payroll’, making the implementation of Payday Super a smooth and easy process.

Why this matters for employers

For many businesses, paying super more frequently will have practical flow‑on effects. Cash flow management may need to be reviewed, particularly for businesses with weekly or fortnightly pay cycles. Payroll processes may also need adjustment to accommodate more frequent super payments and updated reporting requirements.

July 2026 is expected to be a particularly important transition period. During that month, employers may need to manage overlapping obligations, including making the final quarterly super payment for April to June (due by 28 July 2026), while also paying super for each payday from 1 July onwards.

Understanding how these obligations interact will be key to staying compliant, and additionally, there could be a significant cash flow impact for businesses who are not already paying their super every pay cycle. This means that the June 2026 Quarter super as well as July 2026 super may both be payable in July 2026.

Note: Employers should also be aware that the ‘Small Business Clearing house’ is closing. Read the article here for more information

How Mission Advisory can help

Payday Super is a major compliance change, and its impact will differ from business to business depending on payroll structures, pay frequencies and systems in place.

At Mission Advisory, we’re across the upcoming changes and can help you understand what Payday Super means for your business, how it fits with your existing payroll processes, and what needs to change ahead of 1 July 2026.

If you have questions or would like to discuss how these changes apply to your situation, please get in touch with the Mission Advisory team. We’re here to help you navigate the transition with confidence and clarity.